AXA Stock: Updating The Thesis On This French Insurance

VioletaStoimenova

Dear readers,

In this article, we’ll look at AXA (OTCQX:AXAHY) once again. This company has, like most financials, been under a decent amount of share price and valuation pressure. While this of course means we could have invested at a greater upside, that sort of clairvoyance doesn’t really exist, and we need to deal with the situation we have today.

And the situation we have today is an undervalued financial with great fundamentals and a decent amount of upside.

AXA – Let’s revisit French financials

AXA is, as I wrote in my original piece on the company, a great business in the financial sector. The company’s 200+ year history ensures stable fundamentals, at least in theory. The company is an absolute market leader in the insurance market and is among the top/largest insurance companies on earth. It is, at the same time, also one of the world’s largest asset managers, operating under the AXA IM in Europe, and under AllianceBernstein (AB) in the USA.

Yield and upside are the battle cry for investors in AXA such as myself. The current valuation offers an appealing yield of over 7% and that from one of the largest insurance businesses on the planet. The company’s dividend policy calls for a relatively consistent portion of earnings, without much flexibility to establish a dividend tradition or continue one during poor years, as seen in 2019 when the company cut the dividend.

While investors in AXA must accept relatively high amounts of potential volatility – as indicated by the company’s history – this volatility is still offset by a high degree of fundamental safety. AXA has no worrying debt and is A rated or equivalent by every one of the major agencies out there, and has a 2021 solvency II ratio of 217%.

AXA is, to put it simply, a multi-line insurer with decades of experience in the industry.

AXA IR (AXA IR)

Its start as a tiny French operation and its current status as a global leader is a testament to management skills over the past 40-50 years. The company has a historical tendency of focusing on high-growth markets to balance out their mature market incomes (which tend to be lower, but more stable). At the same time, the company is not tied to any one investment and is quick to cut an unprofitable operation from its portfolio when needed. The French giant has also acquired businesses in Colombia, Nigeria, Egypt, Azerbaijan, and Poland, one of the most attractive insurance markets in Central and Eastern Europe.

AXA IR (AXA IR)

In this, AXA shares trends with other French companies, where the business has exposure to what were previously French colonies in Africa. These trends are also found in the telecommunications sector, banking, and other areas. France has a lot of exposure to, and market interest for parts of the African market. I view this as a future advantage.

AXA is still, as of writing this piece, in the midst of a strategic transformation that is going towards its conclusion, which alongside its competitors is a more fee-based model structure. The company’s earnings are now 90%+ fee-based, which is of course an advantage moving into the current environment.

The company’s operations as of 2021 are reported in terms of Property & Casual Insurance, Life & Savings, Health Insurance, and Asset management. There is also a “Holdings & Other segment). Over the past few years, the company has slowly shifted away from a life focus due to the interest rate sensitivity that overexposure to the segment brings. Today, slightly north of half of the company’s earnings, and less than half of the revenues come from the Life segment, with the remainder coming from Non-life and asset management.

AXA IR (AXA IR)

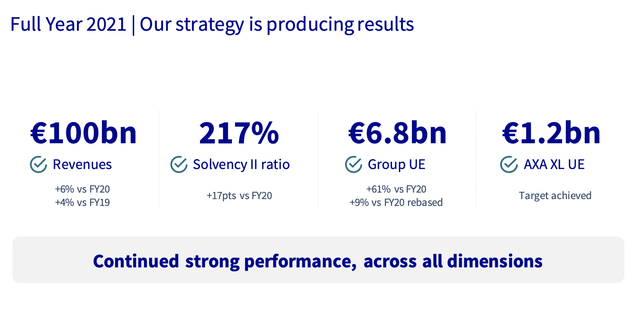

Since all of the company’s segments showed significant growth for 2021 (151% for P&C), this company started out in 2022 with an excellent base market position. RoE saw significant improvements and is now at the high-end of the company’s target range, close to 15%, and the Solvency II ratio increased by almost 17% YoY. The company’s gearing is, as of 2021, less than 27%, with one payment of a Tier 1 debt of $850M in early 2022, and issuance of new debt in early 2022 as well, at what is now considered an excellent cost.

I wrote earlier that it’s fair to consider AXA a French response to the largest insurance company in the world, Allianz (OTCPK:ALIZY). I still view such a comparison as valid and making AXA an interesting investment.

The company’s re-aligning of its portfolio is paying off, with a lower reliance on capital-intensive Savings products and interest-rate-sensitive Life insurance operations. Sales in these legacy segments remain solid, and the company has key market leadership in France here at close to 9% of the entire market, as well as 10% of the Swiss and almost 8% of the Belgian market. It lacks the German market focus that Allianz has – but we don’t need it. We have Allianz for that.

AXA IR (AXA IR)

By investing in AXA we get appealing exposure to strong European markets that we don’t get as much with Allianz.

The trends in Health insurance are what drive the company’s segments in this area. We’re seeing a shift from individual coverage/policies to group policies due to the introduction of compulsory corporate health coverage, even if this is somewhat still dependent on how individual nations as the development isn’t 1-1 everywhere.

Through the XL M&A, AXA is now the world’s leading P&C Commercial lines insurer, and is integral to the company’s shift from life to a broader portfolio composition.

While the asset management business seems small, it actually generates over €2B in revenues and has over €804B in AUM. AXA is, because of this, among the 20 largest asset managers in the entire world. This branch of AXA is in need of growth and scale, and Allianz is significantly ahead of AXA in this.

The company also outperforms on other levels, such as generating significant capital above guidance for 2021, and with over €4.4B in cash in holding, preparing it well for the cataclysm that has been the 1H22 in Europe due to a mix of macro and other trends.

The fact is that AXA has dropped 21.7% since my last article, underperforming most indices. My position is still green, because I bought my AXA at dirt-cheap valuations inclusive of dividends and FX. However, I believe the market is now severely mispricing AXA and its future potential.

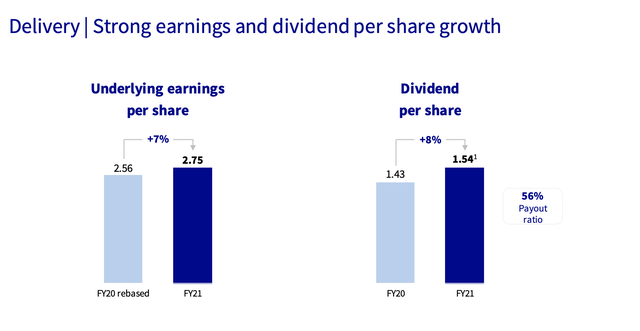

This is the power of valuation-centric dividend investing. Now, my position was initially about €7,000 – and up about 95% including dividends and FX. When looking at AXA today, we’re seeing a very resilient company despite potentially unfavorable economic trends in the near future. The dividend yield is also offering an upside potential, thanks to a higher dividend and given the new payout range at 50-60% of adjusted earnings. With XL included, we should see continued growth in that dividend for the next few years or so.

(Seeking Alpha, AXA article)

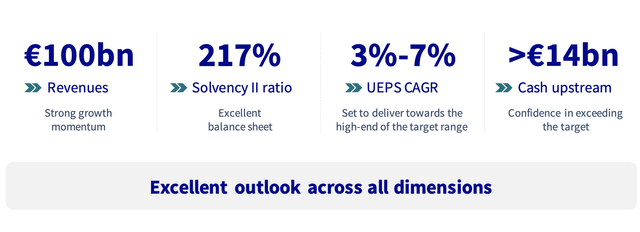

Because as the company’s own forecasts suggest, this is not a downtrend valuation based on poor earnings going forward, but one contrary to the expected trend.

AXA expects earnings growth for 2022E, and analysts agree. S&P Global forecasts a 2% 2022E EPS growth, and FactSet is at 1.8%, calling for the ADR to generate $3.11 EPS for the fiscal.

Let’s look at what exactly this would mean for the valuation.

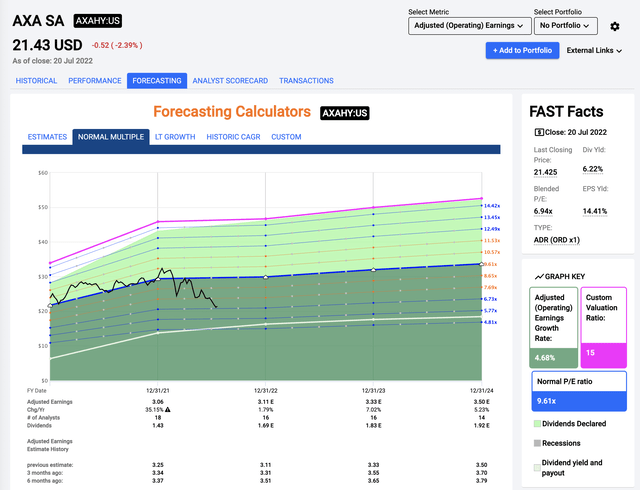

AXA’s valuation

If we’re to believe the market’s assessment of AXA, then the market believes the company to be worth no more than 6.94X P/E, for a 7%-yielding insurance business with an A grade credit rating. A bit steep if you ask me, especially since the company typically trades at least 3X P/E above that.

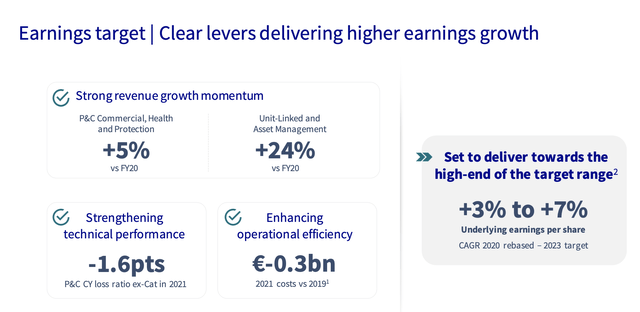

2023-2024E are not expected to be paltry years either, with EPS growth of 5-7% on the high end, which would suggest a significant undervaluation at this particular juncture.

AXA valuation (F.A.S.T graphs)

The company typically doesn’t stay at these sorts of valuation ranges for very long. While it’s entirely possible for us to go deeper “down south” here, I don’t see the fundamental risk to this if you’re investing long-term. As a long-term investment, this company has a significant upside. Even to just a 10X P/E, that upside is 28% annually, or close to 80% total RoR to 2024E targets. That’s alpha, as I see it.

Even if the company were to trade flat around that 6-8X P/E, the upside is 10-15% annually or 30-40%, and that’s in flat trading for the next few years.

Based on this valuation, there are very few scenarios that I see where the company would result in a long-term negative RoR. On a peer basis, AXA’s closest peers are Allianz (OTCPK:ALIZF), Zurich (OTCQX:ZURVY), Generali (OTCPK:ARZGY), and Sampo (SAXPY). In this group, the average P/E lies close to 11-12X – AXA is undervalued to this multiple – and is also undervalued to P/B multiples, and offers a higher yield than all of its competitors at current valuations. From a peer-based perspective, the company is now at a deep discount to averages, with the highest discount in P/B.

The average at this time is around €30.5/share, and 19 out of 20 analysts consider the company either a “BUY” or an “Outperform”. This target has not shifted for over 5 months – not on average. While I would say the €30.5 price is justifiable –I would go lower to a €28.5/share price target, more in line with a fair-value peer average.

But even on such a target basis, the current undervaluation we see in AXA is very significant. I would say it’s close to 40% here, and AXA should be considered one of the primary buys if you’re a conservative dividend investor.

Thesis

My thesis for AXA is as follows:

- This is one of the largest asset managers and insurers in all of Europe and the world. It has rock-solid foundations and a 200-year history. Under the right circumstances and at the right valuation, this company is a definite “BUY”.

- I believe that a conservative estimate of the company’s abilities calls for at least a target of €28.5/share, which would imply a 35%+ upside for the company based on where I trade today.

- Based on this, I would consider AXA a “BUY” here.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Chemours Company is currently a “BUY”.